GLP-1 Insurance Coverage: Prior Authorization and Appeal Checklist

Edited by Ryan Lafayette. Coverage and prior-auth rules vary by plan, so we organize public details readers should confirm with their plan or provider. Not medical advice.

SHORT ANSWER

Your plan decides whether a GLP-1 is covered. It may look at the diagnosis, the drug requested, and rules such as prior authorization, step therapy, or an appeal.

- The trap A provider saying "we help with insurance" does not mean your plan will approve the medication or cover the final cost.

- The fix Check the benefit category, formulary, prior authorization rules, and denial reason before you spend time on the wrong appeal.

- Best next step Keep the insurance review moving. At the same time, compare paying out of pocket if timing or cost uncertainty matters.

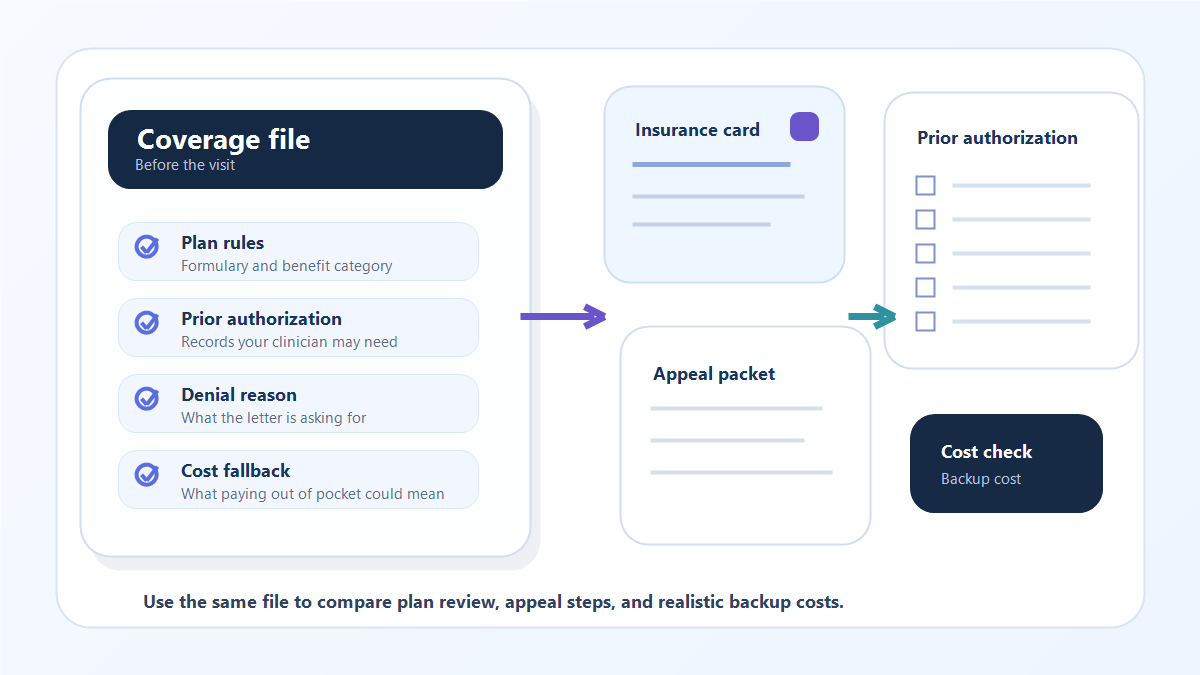

Use this article when you need a practical GLP-1 insurance coverage checklist. It shows what to ask your plan, what your clinician may need for prior authorization, how to read a denial letter, and when to compare paying out of pocket while insurance review continues.

Coverage details guide

This page organizes public coverage, prior-auth, plan-rule, and provider-support details so readers know what to confirm with their plan or provider. Not medical advice.

If you are still deciding how to get the prescription, the GLP-1 access options guide separates clinical intake, telehealth, insurance, paying out of pocket, and pharmacy fulfillment before you choose an option.

If insurance timing or final cost is still unclear, use the Compare Tool to check current provider options while you keep the coverage review moving.

For the broader coverage hub, start with Insurance & Coverage. This page goes deeper on the checklist and appeal-prep side.

Watch: insurance support is not approval

This short explainer shows how to read insurance-support language, prior authorization help, and plan-dependent pricing without treating them as guaranteed approval.

Video chapters

What Insurance Can Check Before It Says Yes

Before a GLP-1 prescription is covered, the plan may check three things. It may ask whether weight-management medication is covered, whether the requested drug is on the formulary, and whether the request meets prior authorization rules.

- Benefit category. Some plans cover weight-management medications. Others exclude them or cover GLP-1s only for a different diagnosis.

- Formulary status. The plan may cover one medication, require another first, or apply different rules to different doses.

- Prior authorization. A plan may require documentation before it decides whether the prescription meets its medical-necessity rules.

- Step therapy. The plan may ask for records showing prior treatment attempts before it reviews the requested medication.

- Cost sharing. Even after approval, your deductible, copay, coinsurance, and pharmacy rules can still affect what you pay.

Preauthorization is a plan decision about whether a treatment or drug is medically necessary under the plan's rules. It is not a promise that all costs are covered, so the price question still needs its own check.

What to Ask Your Plan Before the Visit

Use the member services number on your insurance card and ask for the current plan-year rules. Take notes during the call, including the date, representative name, and any reference number.

| Question to Ask | Why It Matters |

|---|---|

| Does my plan cover weight-management medications? | This separates a possible paperwork problem from a plan exclusion. |

| Which GLP-1 drugs and doses are on the formulary for my diagnosis? | Ozempic, Wegovy, Mounjaro, and Zepbound can be handled differently because the diagnosis and label may differ. |

| Is prior authorization required? | If yes, your clinician needs to submit the required records before the plan reviews the request. |

| What documentation is required? | The plan may ask for BMI, diagnosis, past treatment attempts, step therapy, or program participation records. |

| If approved, what would I pay? | Approval does not erase deductibles, copays, coinsurance, or pharmacy rules. |

| What is the appeal deadline if the request is denied? | Appeals usually have deadlines. Missing the deadline can close off options. |

Start Quiz

Find your best GLP-1 match

What should the Compare Tool check first?

Checking coverage next?

Compare insurance supportWhat Usually Belongs in the Prior Authorization File

There is no universal GLP-1 prior authorization checklist. The useful move is to match the file to the exact plan rule. These are the records plans commonly ask for when weight-management coverage is available.

- Current measurements. Height, weight, BMI, and the date they were recorded.

- Diagnosis and related conditions. Chart notes, labs, or diagnoses that explain why the medication was prescribed.

- Past treatment attempts. Prior medications, nutrition counseling, lifestyle program records, or other therapies the plan requires before approval.

- Medication requested. Drug name, dose, diagnosis, and why that drug is being requested instead of another option.

- Supporting chart notes. A clear record from the clinician connecting the plan rule to the documentation submitted.

If you are switching providers or filling gaps from an earlier visit, use the GLP-1 medical records request checklist before the appeal or resubmission. A stronger file starts with the records the next clinician can actually review.

What to Do With a Denial Letter

A denial letter is not just a no. It should tell you why the plan refused the request and what appeal options are available. Read it before deciding whether to appeal, resubmit, or compare paying out of pocket.

- Find the stated reason. Look for missing records, step therapy, a formulary issue, a diagnosis mismatch, or a plan exclusion.

- Ask for the plan rule. Request the clinical policy or coverage criteria used to make the decision.

- Fix the specific gap. Do not resubmit the same file if the denial says a document, diagnosis, or prior treatment history is missing.

- Submit the internal appeal on time. Follow the plan's instructions exactly, including forms, deadlines, and supporting documents.

- Check external review rights. Some denials can be reviewed by an independent third party after internal appeal steps.

If the denial says the plan does not cover weight-management medication at all, ask whether any exception process exists. If there is no usable exception, the more practical next step may be comparing the cost of paying out of pocket while you decide whether to keep appealing.

Employer, Medicare, and Medicaid Rules Are Different

Do not assume one person's approval predicts yours. The same insurer name can sit on top of very different benefits.

- Employer and individual plans. Employer plan design can decide whether weight-management drugs are included, excluded, or handled through extra clinical rules.

- Federal employee plans. Plan-year documents matter. Check current benefit materials rather than relying on an old brochure or screenshot.

- Medicare. Medicare has separate 2026 GLP-1 policy context. Do not treat Medicare Part D or Medicare Advantage rules as the same as commercial insurance.

- Medicaid. Medicaid GLP-1 coverage can vary by state, diagnosis, and program. Current state or managed-care plan guidance matters more than old state examples.

This is why the safest question is not "Does insurance cover GLP-1s?" It is "Does my current plan cover this drug for this diagnosis, and what does it require before approval?"

When to compare paying out of pocket

Comparing paying out of pocket does not mean giving up on insurance. It keeps two questions separate. First, your plan may still review the medication. Second, you can decide whether a non-covered option is affordable if the review takes too long or fails.

- Timing matters. Prior authorization and appeals can take time, especially if records are missing.

- The denial looks like an exclusion. A paperwork denial may be fixable. A plan exclusion may require a different cost plan.

- The approved cost is still unclear. Approval can still leave deductibles, coinsurance, or pharmacy rules.

When you compare paying out of pocket, look beyond the first advertised price. Separate membership fees, medication cost, intro pricing, ongoing refill cost, and cancellation terms. The GLP-1 provider pricing guide explains how to read those costs before you choose.

If the out-of-pocket option is a manufacturer-linked pharmacy fill, check what is included. The NovoCare Wegovy Pharmacy guide can help you separate medication price and delivery from prescribing care.

Quick FAQ

Does prior authorization mean my GLP-1 will be paid for?

No. Prior authorization means the plan reviewed the request under its rules. You may still owe deductibles, copays, coinsurance, or other cost sharing.

Why was I denied if my clinician prescribed the medication?

The plan may be applying a benefit exclusion, formulary rule, step therapy requirement, missing documentation rule, or diagnosis requirement. The denial reason tells you which problem to solve first.

Should I appeal every denial?

Appeal when the denial can be answered with better documentation, corrected diagnosis details, or plan-rule evidence. If the plan has a firm exclusion and no exception process, comparing paying out of pocket may be more useful than repeating the same request.

Can insurance help from a telehealth provider guarantee approval?

No. Insurance help may mean benefit checks, prior authorization paperwork, or appeal support. Your insurer still makes the coverage decision.

Medical disclaimer: This article is educational and is not medical, legal, or insurance advice. Coverage rules change by plan and plan year. Verify benefits directly with your insurer, review your current plan document, and work with your clinician on medical documentation and appeal decisions.

References

- NAIC. Does Insurance Cover Prescription Weight-Loss Injectables? Back to top

- HealthCare.gov. Preauthorization. Back to top

- HealthCare.gov. Appeal an insurance company decision. Back to top

- CMS. Medicare GLP-1 Bridge. Back to top

- KFF. Medicaid Coverage of and Spending on GLP-1s. Back to top

- Aetna. GLP-1 benefits and coverage for employers. Back to top

- FEP Blue. Plan brochures. Back to top